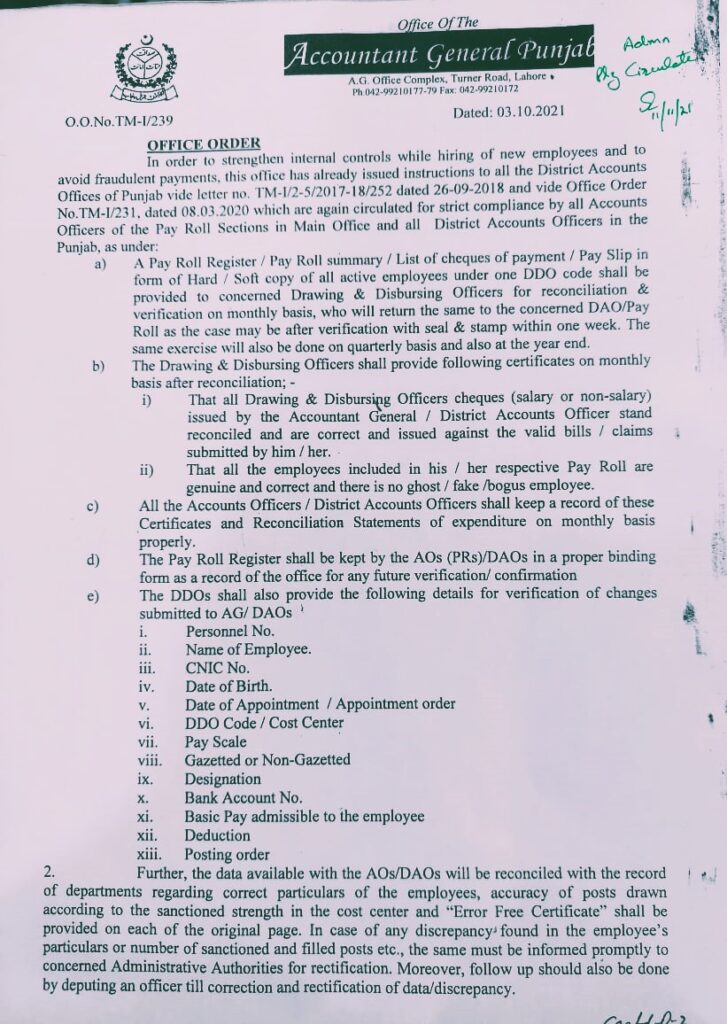

Verification of Payroll by the DDOs -AG 03.10.2021

In light of the importance of maintaining stringent internal controls, the Accountant General’s office has issued clear and updated instructions on the verification of payroll. This guide elaborates on the essential duties and procedures that Drawing and Disbursing Officers (DDOs) must follow, as detailed in the recent office order dated October 3, 2021. The aim of this directive is to strengthen internal controls, prevent fraudulent payments, and ensure the accuracy of payroll records.

Overview of the Office Order

The Office Order No. TM-1/239 issued on October 3, 2021, serves as a reinforcement of previous guidelines for payroll verification. This directive, which builds on earlier instructions from September 26, 2018, and March 8, 2020, sets forth a series of procedures that all Accounts Officers in the Payroll Sections of Main Offices and District Accounts Offices (DAOs) in Punjab must follow to ensure the integrity of payroll management.

Key Responsibilities for DDOs in Payroll Verification

The order mandates a series of tasks and certifications that DDOs must perform to comply with payroll verification standards:

- Monthly Reconciliation and Verification:Every month, the DDOs are required to reconcile and verify the following documents:

- Pay Roll Register: A comprehensive summary or list of cheques issued for payments to employees.

- Pay Roll Summary: An overview of all active employees under the DDO code.

- Pay Slips: Hard or soft copies detailing the salaries of employees.

- Quarterly and Year-End Reconciliation:In addition to the monthly tasks, DDOs must also perform reconciliation on a quarterly basis and at the end of the year. This additional layer of verification helps maintain the accuracy of the payroll records over a more extended period and ensures that annual records are up-to-date.

- Monthly Certification:DDOs are required to provide the following certifications on a monthly basis:

- Verification of Cheques: Confirm that all cheques issued for salary or non-salary claims are correctly reconciled and were issued against valid bills or claims.

- Employee Verification: Ensure that all employees listed in the payroll are genuine, with no instances of ghost or bogus employees.

- Documentation and Record Keeping:Accounts Officers/DAOs must maintain a record of these certifications and reconciliation statements. Proper documentation ensures that there is a reliable record of all payroll activities for future audits or reviews.

- Pay Roll Register Maintenance: The Pay Roll Register must be kept in a properly bound format for reference and future verification.

- Verification of Employee Details:The DDOs must provide detailed information for the verification of changes submitted to the Accountant General/DAOs, including:

- Personnel Number

- Name of Employee

- CNIC Number

- Date of Birth

- Date of Appointment/Appointment Order

- DDO Code/Cost Center

- Pay Scale

- Gazetted or Non-Gazetted Status

- Designation

- Bank Account Number

- Basic Pay Admissible

- Deductions

- Posting Order

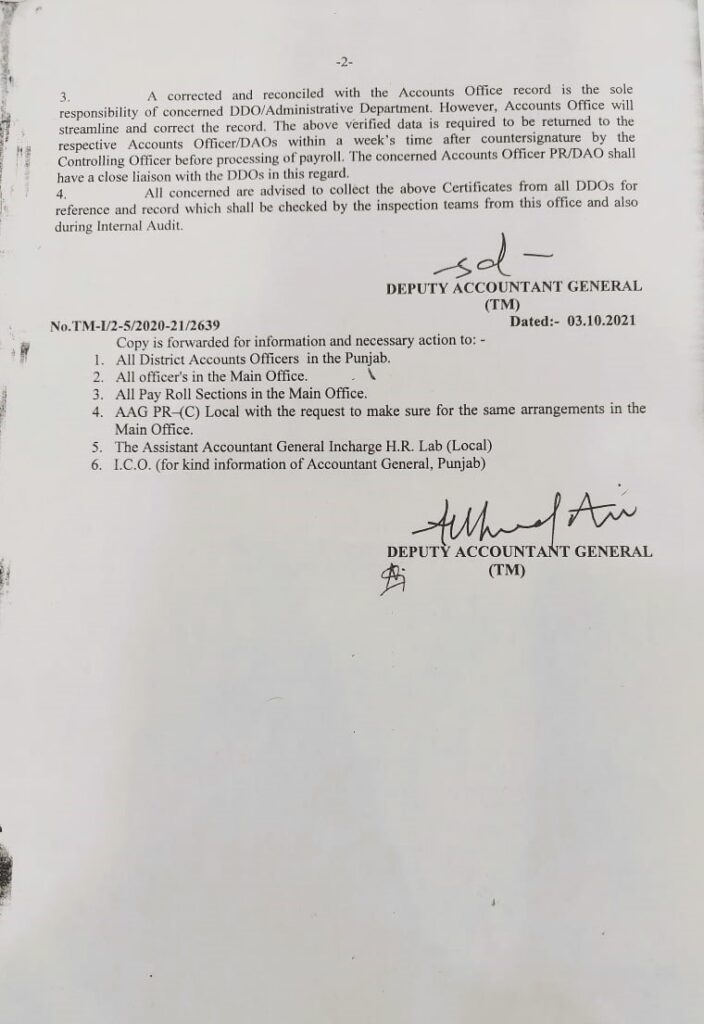

- Data Reconciliation and Error-Free Certification:The data maintained by the AOs/DAOs must be reconciled with departmental records to confirm the accuracy of employee details and sanctioned posts. Any discrepancies must be reported to administrative authorities for correction.

- Error-Free Certificate: An “Error-Free Certificate” must be provided on each original page of the records, signifying that all entries are correct.

- Follow-Up on Corrections: An officer must be deputed to follow up on discrepancies until all corrections are made.

Why is Payroll Verification Important?

Payroll verification is not merely a procedural task but a fundamental aspect of financial management that impacts several key areas:

- Prevention of Fraud:Rigorous payroll verification helps detect and prevent fraudulent activities such as ghost employees or unauthorized salary payments. By ensuring that every payment is justified and documented, the risk of financial misconduct is significantly reduced.

- Maintaining Financial Integrity:Accurate payroll records uphold the financial integrity of the institution. Regular checks and certifications ensure that the payroll system functions as intended and that all transactions are legitimate.

- Ensuring Compliance:Adhering to the verification procedures ensures compliance with legal and regulatory requirements. This compliance is crucial for maintaining the trust of stakeholders and fulfilling the obligations set forth by the Accountant General’s office.

- Facilitating Audits:Well-maintained records and certifications streamline the audit process. When payroll records are accurate and complete, audits are more efficient and effective.

Best Practices for Effective Payroll Verification

To ensure compliance with Rule 4.49(a) and maintain high standards in payroll management, DDOs should follow these best practices:

- Adherence to Timelines:Strictly follow the timelines for monthly, quarterly, and year-end reconciliations and certifications.

- Accuracy in Documentation:Ensure that all documents are accurately completed and that all required details are included.

- Regular Training:Engage in regular training sessions to stay updated on best practices and any changes to regulations.

- Effective Communication:Maintain open lines of communication with the DAO/Payroll Section to resolve any issues or discrepancies promptly.

- Thorough Review Processes:Implement a thorough review process for all payroll-related documents to ensure accuracy and prevent errors.

Conclusion

The verification of payroll by DDOs is a critical responsibility that ensures the integrity, transparency, and effectiveness of the payroll management system. By adhering to the procedures outlined in Office Order No. TM-1/239 and following best practices, DDOs can contribute to a robust financial management framework that upholds public trust and regulatory compliance.

The guidance provided in this office order underscores the importance of diligent verification processes and reinforces the need for accountability in the handling of government funds.

By implementing these procedures effectively, all Accounts Officers and DDOs in Punjab can help maintain a high standard of financial integrity and prevent any potential misuse of public resources.